By: Iqbal Aji Harjuna and Stephen Shiwei Wang

Edited By: Sayidcali Ahmed

Introduction

For emerging markets, rapid fintech expansion often unfolds against a backdrop of incomplete regulatory frameworks and uneven institutional capacity. Emerging markets are economies in transition from low- to middle-income status, characterized by rapid growth and transformation. While integrating into the global economy, they face specific challenges, including legal uncertainties, limited liquidity, and unpredictable regulatory compliance.1 In the context of fintech development and other new and emerging industries, these economies have less systemic, meaning institutional, approaches to regulating information. This relates to the developmental capacity of 1) suppliers’ compliance and growth and 2) demand-side salience toward new products. These economies exhibit unpredictable legal and regulatory structures concerning the management of information, which directly affects the developmental capacity of 1) regulatory compliance for suppliers and 2) the growth of the consumer market and domestic demand for innovative products.

Fast development and incomplete regulatory systems can lead to regulatory shocks. China’s crackdown on the fintech sector in 2020 illustrates the role and power of government regulations in emerging economies when financial innovation generates systemic and social risks. A weak form of regulatory institution is not a weak force of regulation; it is instead an unpredictable form of regulatory force.

Rapid industrialization and the implementation of modern technologies can result in significant regulatory shocks. The 2020 intervention in the Chinese fintech sector demonstrates that legal and regulatory compliance in emerging economies is often characterized by heightened political and social risk. Therefore, a weak institutional framework does not signify a lack of authority but an unpredictable form of regulation.

A general idea in development economics is that financial development should follow “slow and steady growth.” Reducing the number of shocks in emerging economies is a crucial aim in the study of emerging markets. As Indonesia’s fintech industry continues to expand, the question is whether it will become a second China, adopting stringent regulatory interventions.

This question is especially relevant given the similarities between Indonesia’s current fintech trajectory and China’s experience prior to 2020. In both cases, fintech growth has been driven by rapid digital adoption, low entry barriers, and unmet demand for financial services outside traditional banking. However, the Chinese crackdown was not a rejection of fintech itself, but a response to mounting financial instability and social unrest. Whether Indonesia is approaching a comparable threshold remains uncertain.

China Fintech Overview

China’s fintech sector expanded rapidly after 2013, fueled by widespread internet use, which accounted for 53.2 percent of the population, and by the rise of large digital platforms with an annual growth rate of ten percent. Third-party payments, online consumer finance, and P2P lending grew quickly, initially enhancing financial inclusion through small loans with short maturities. Regulatory oversight during this period relied primarily on fragmented and nonbinding policy guidance rather than enforceable legal frameworks.² As a result, risks accumulated beneath the surface, particularly in the lending market.

Over time, these weaknesses became increasingly visible. Many P2P platforms engaged in risky or deceptive practices, including implicit guarantees to investors and opaque fund usage, which exacerbated information asymmetry and moral hazard.³ Some platforms operated as underground banks or Ponzi schemes, generating significant systemic and social risks.⁴ When thousands of platforms collapsed, investor losses and social protests followed, prompting the Chinese government to intervene in the name of financial stability and social order.

Indonesia Fintech Overview

Indonesia’s fintech market has followed a different trajectory. The country’s large population, rising smartphone penetration, and sizable unbanked segments have created strong demand for digital financial services. Fintech platforms, especially in payments and P2P lending, have helped fill gaps left by traditional banks, particularly for micro, small, and medium enterprises. Fintech has therefore become closely linked to Indonesia’s broader financial inclusion agenda.

Unlike China’s pre‑2020 approach, Indonesia introduced baseline regulations for P2P lending relatively early. The Financial Services Authority (OJK) established licensing, transparency, and capital requirements in 2016, and subsequently strengthened governance standards as the market expanded. Interest and fee caps were later introduced, and thousands of illegal lending platforms were shut down.⁵ These measures indicate a supervisory approach aimed at containing risk without suppressing innovation.

Market Conditions for the Fintech Industry

Fintech and traditional banking share the same market. Indonesia has large credit gaps for MSMEs, expensive banking services, a sizable informal economy, and limited access to formal loans. Fintech has lower barriers to entry, lower transaction costs, and alternative credit rating methods that help fill these demand gaps, making it particularly attractive to underserved consumers.

Fintech also relies on technologies such as mobile networks, digital payments, e‑commerce ecosystems, and big data, which collectively form platforms that enable downstream services to expand easily. In China, Alipay and WeChat created digital ecosystems that support a full range of financial services, including lending, saving, and investment. Indonesia has built similar ecosystems through Gojek, Tokopedia, and Shopee. Platform-based service development accelerates fintech expansion. Fintech markets also experience strong network effects. In payments, a few major players dominate, while in P2P lending, many platforms initially enter due to low entry barriers. Over time, weaker platforms exit or fail, leading to market consolidation.⁶

A Market Reform Framework

Institutional views suggest that regulatory forces depend on two dimensions: government capacity and industry risk. Government capacity refers to the government’s ability to monitor, enforce, and restructure financial markets, while industry risk captures the extent to which localized market failures could threaten financial stability. Different starting conditions determine how market reforms unfold. Countries with high fintech risk and high government capacity tend to adopt stricter intervention, similar to China’s actions during the P2P crisis. Moderate risk combined with medium or limited capacity results in partial regulation and gradual adjustments, consistent with Indonesia’s approach. This means Indonesia regulates fintech in smaller steps because regulators face manageable risks and possess moderate enforcement resources. China regulated more aggressively because risks became systemic at a time when regulatory capacity was strong enough to enforce rapid reforms.

Market Failure

Market failure risks remain central to this comparison because emerging economies often have less transparent information systems. Fintech lending is vulnerable to information asymmetry, moral hazard, and negative externalities such as over-indebtedness and abusive collection practices. In China, these failures spread rapidly and overwhelmed existing safeguards, turning consumer-level problems into systemic threats. Regulatory intervention became unavoidable once social costs escalated. In Indonesia, similar risks exist but remain more contained. Improvements in digital credit scoring, mandatory licensing, governance requirements, and interest caps have reduced adverse selection and opportunistic behavior among platforms. Evidence suggests that fintech lending in Indonesia has not increased instability in the banking sector and may even complement formal credit markets by improving borrower screening.

Required Demand-Supply Conditions for Fintech to Flourish

High economic equilibria require supportive demand and supply conditions. On the demand side, both countries have large populations with rapidly growing digital user bases, and smartphone adoption has boosted mobile payments and online lending. Digital lifestyle normalization has further increased demand for mobile payments and online financing. Demand also comes from consumers excluded from traditional banking, creating a deadweight loss when transactions that should occur do not.

On the supply side, fintech grows when platforms aggregate multiple services into centralized apps that leverage existing user flows and brand familiarity. Government supervision also shapes supply. States with lower capacity tend to allow fintech activity to expand to promote innovation, whereas states with higher capacity enforce stricter rules to limit risks. The supply of P2P lending is directly shaped by regulatory stances.

Indonesia has strong demand and moderate supply in the fintech market due to its rising population, normalizing digital lifestyles, and significant financial exclusion. Indonesian fintech companies possess strong platforms offering bundled financial services. The Indonesian government adopts a facilitative regulatory approach because state capacity is relatively low, and it acted early to establish clear laws defining acceptable P2P lending practices. The enforcement of standards limits lending malpractice.

China had strong demand and supply before 2020. Its population had deeply integrated Alipay and WeChat into daily life, and China had the lowest formal credit usage among BRICS at around 6.5 percent, leading many people to informal borrowing.⁷ The supply of fintech services in China was shaped by strong platforms and, according to institutional theory, high state capacity. By definition, regulations should have been stronger, but the government did not enact a strong regulatory stance on fintech until 2020.⁸

Market Failures and Regulatory Stances

Market failures can distort demand and supply equilibria and scale into social instability. Governments intervene to maintain political and social stability, and when market failures threaten the social order, they become systemic risks. China’s P2P market caused widespread social instability as platforms failed and Ponzi schemes emerged. Many platforms acted as underground banks and posed as P2P intermediaries, offering guarantees that contradicted P2P principles.⁹ These were clear cases of information asymmetry. Platforms exploited opportunism and assumed excessive risks because they did not bear full consequences. They delivered guaranteed high returns to attract investors, aggressively extending debt. This led to suicides and protests.

Evidence shows that Indonesian platforms have reduced information asymmetry and adverse selection through improved digital credit scoring and wider use of borrower data.¹⁰ OJK responded early with policies such as POJK 77/2016, which established basic licensing, transparency, and data obligations, and POJK 10/2022, which strengthened governance, increased minimum capital, and required stricter fit-and-proper assessments for managers.¹¹ Indonesia also introduced interest and fee caps in 2023 and removed thousands of illegal lenders through the Investment Alert Task Force to limit over-indebtedness and abusive collection practices. Evidence on systemic risk shows that Indonesian fintech lending does not increase bank instability. Instead, it improves bank screening and is associated with lower credit risk in the formal banking sector.¹² This suggests that Indonesia’s risks remain below the systemic threshold described in the Reform Process Matrix. Indonesia faces real market failures, but they are not widespread enough to justify a Chinese-style intervention.

Conclusion

Indonesia is unlikely to become a second China in its P2P lending regulations. The direct reasons for China’s 2020 fintech crackdown were social instability driven by rapid growth in P2P lending platforms and aggressive lending practices. The spurious growth of P2P platforms increased opportunities for Ponzi schemes to pose as intermediaries, undermining market trust, and aggressive lending practices intensified default rates, fueling social instability. Indonesia’s P2P sector has seen slower supply growth compared to China’s pre‑2020 period, and regulators intervened earlier with licensing, reporting, and interest-rate controls. As a result, Indonesia’s current P2P risks are primarily consumer protection issues rather than social or systemic instability. Given differences in institutional logics, regulatory capacity, market equilibria, and risk levels, Indonesia’s regulation of the P2P lending sector is unlikely to tighten in the same manner as China’s. Its regulatory adjustments are expected to continue following a gradual and supervisory approach rather than a sweeping restriction.

Appendix A

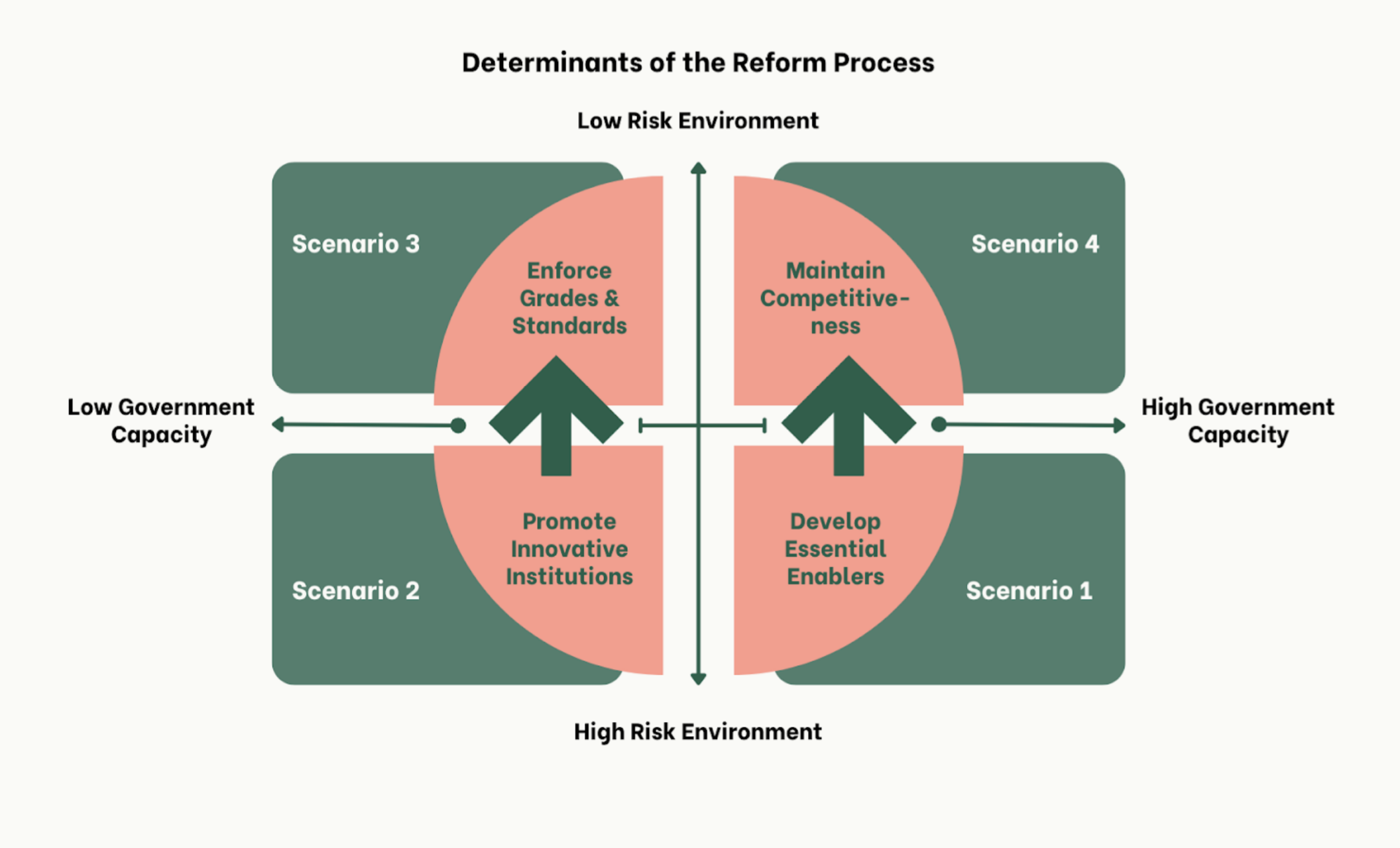

Note: Adapted from Christy, R. D. 2025. Week 3: The legal foundation and institutions for market-based economics [PowerPoint slides]. AEM 4420: Emerging Markets (2025FA), Cornell University.

This figure illustrates key determinants that shape the success and type of policy reform required. The vertical axis represents the Risk Environment (ranging from Low to High) and reflects market volatility, systemic instability, or public opposition. The horizontal axis represents Government Capacity (ranging from Low to High), reflecting the state’s technical, administrative, and political ability to design and implement policy.

The four scenarios derived from the model are:

Scenario 1 (high risk, high government capacity) emphasizes the need to develop essential enablers to manage instability and support necessary reforms.

Scenario 2 (high risk, low government capacity) focuses on promoting innovative institutions that can compensate for limited state capacity.

Scenario 3 (low risk, low government capacity) suggests enforcing grades and standards as a minimal yet necessary governance function.

Scenario 4 (low risk, high government capacity) seeks to maintain competitiveness through continued institutional strength and policy effectiveness.

Work Cited

- Rubaj, P. 2023. Emerging Markets as Key Drivers of the Global Economy. European Research Studies Journal, XXVI(4), 431–445. https://doi.org/10.35808/ersj/3294.

- Yuan, K., & Xu, D. 2020. Legal Governance on Fintech Risks: Effects and Lessons from China. Asian Journal of Law and Society, 7(2), 275–304. doi:10.1017/als.2020.14.

- Mardjono, A., & Setyawan, I. R. 2025. Moral Hazard, Adverse Selection, and Capital Structure in Fintech Microfinance in Indonesia. Journal of Posthumanism, 5(3), 684–691. https://posthumanism.co.uk/jp/article/view/777.

- Chorzempa, M. 2018. Massive P2P Failures in China: Underground banks Going Under. China Economic Watch. Peterson Institute for International Economics. https://www.piie.com/blogs/china-economic-watch/massive-p2p-failures-china-underground-banks-going-under.

- Hadi, A. 2023. OJK imposes cuts on P2P interest rates, fees starting next year. The Jakarta Post. Published November 10. https://www.thejakartapost.com/business/2023/11/10/ojk-imposes-cuts-on-p2p-interest-rates-fees-starting-next-year.html.

- Zetzsche, D. A., Buckley, R. P., Arner, D. W., & Barberis, J. N. 2017. Regulating a revolution: From regulatory sandboxes to smart regulation. Journal of Financial Regulation and Compliance, 23(1), 1–27. https://ir.lawnet.fordham.edu/jcfl/vol23/iss1/2/.

- Fungáčová, Z., & Weill, L. 2015. Understanding financial inclusion in China. China Economic Review, 34, 196-206.

- Chorzempa, M. 2018. Massive P2P Failures in China: Underground banks Going Under. China Economic Watch. Peterson Institute for International Economics. Published August 21. https://www.piie.com/blogs/china-economic-watch/massive-p2p-failures-china-underground-banks-going-under.

- Ibid.

- Mardjono, A., & Setyawan, I. R. 2025. Moral hazard, adverse selection, and capital structure in fintech microfinance in Indonesia. Journal of Posthumanism, 5(3), 684–691. https://posthumanism.co.uk/jp/article/view/777.

- OJK. 2022. Peraturan OJK No. 10/POJK.05/2022 tentang Layanan Pendanaan Bersama Berbasis Teknologi Informasi. https://ojk.go.id/id/regulasi/Documents/Pages/Layanan-Pendanaan-Bersama-Berbasis-Teknologi-Informasi/POJK%2010%20-%2005%20-%202022.pdf.

- Junarsin, E., Pelawi, R. Y., Kristanto, J., Marcelin, I., & Pelawi, J. B. 2023. Does fintech lending expansion disturb financial system stability? Evidence from Indonesia. Heliyon, 9, e18384. https://www.sciencedirect.com/science/article/pii/S2405844023055925.

Author Bio

Iqbal Aji Harjuna is a second-year MPA student at the Cornell University’s Brooks School of Public Policy, focusing on International Development with a specialization in Environmental Finance and Impact Investing. He has worked at Indonesia’s Ministry of Finance for ten years, where he has been involved in policy implementation and enforcement. His professional experience includes assignments at Indonesia’s largest international port and a major international airport, where he facilitated trade and industry, strengthened border protection, and examined the effectiveness of research in improving stakeholder compliance. With an academic background that bridges frontline enforcement and policy analysis, Iqbal is committed to strengthening public sector performance. Upon graduation, he plans to return to Indonesia’s customs administration to apply the analytical tools and global perspectives gained from his studies to advance institutional reform and promote accountable and resilient governance.